Here's a scenario that shatters the intuitions of most new traders: you have a strategy with a 55% win rate and a 1.5:1 reward-to-risk ratio. Your expected value per trade is clearly positive. You are mathematically profitable. Now you risk 25% of your account on each trade. Question: what is your probability of losing 90% of your account within the first 100 trades? The answer — which almost everyone gets dramatically wrong — is approximately 97%. This is the risk of ruin: the mathematical certainty that even profitable strategies, bet too large, eventually destroy the account that implements them. Understanding this concept is not optional for serious traders. It is the mathematical bedrock upon which all sustainable trading is built.

What Risk of Ruin Is and Why It's Non-Negotiable Mathematics

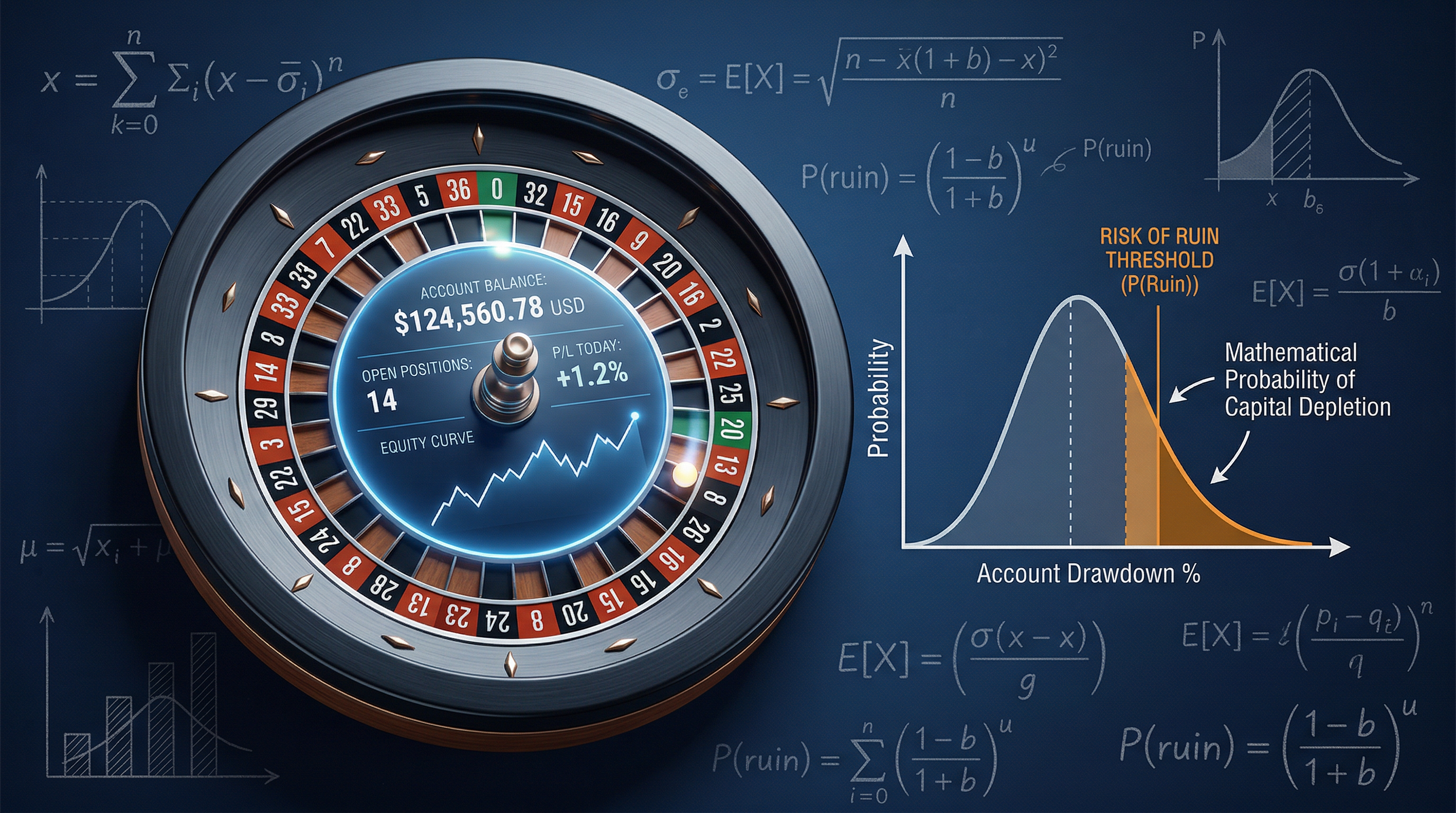

Risk of Ruin (RoR) is the probability that a trader will lose enough of their capital to prevent continued trading — the "ruin" threshold. It is calculated from three inputs: win rate (W), average reward-to-risk ratio (R), and position size as a fraction of account (f). The mathematics, derived from probability theory and the gambler's ruin problem, produce a result that is often shocking: even strongly positive-expectancy strategies have high ruin probabilities at large position sizes.

A simplified RoR formula: RoR ≈ ((1-Edge) / (1+Edge))^(N), where Edge = W×R - (1-W). For most retail trading strategies, realistic position sizes above 5-10% of account create ruin probabilities that are unacceptably high over multi-year trading horizons — regardless of how good the strategy actually is.

The Kelly Criterion Connection: Optimal Bet Sizing Exists

The Kelly Criterion, derived by John Kelly at Bell Labs in 1956, provides the mathematically optimal position size for maximizing geometric growth while managing ruin risk. Full Kelly sizing maximizes long-term returns but allows large short-term drawdowns. Most professional applications use fractional Kelly (25-50%) to reduce variance while preserving most of the edge. Traderise's position sizing tools incorporate Kelly-based calculations to help traders find the mathematically sound position size for their specific strategy statistics.

The psychological temptation to bet large when you're confident is understandable — but confidence and correct position sizing are completely different calculations. A 90% confident trader who bets 20% of their account per trade has a far higher ruin probability than a 55% confident trader who bets 1% per trade, over any realistic time horizon. Traderise's risk controls enforce position size limits that keep your RoR at manageable levels even during your most confident periods.

The 5 Most Common Ruin Traps Retail Traders Fall Into

1. The "I'm Up, I Can Afford to Risk More" Trap

After a profitable period, traders often increase position sizes, reasoning that recent profits provide a buffer for larger bets. But the math is unforgiving: RoR calculations apply to your current account value regardless of where those funds came from. A $15,000 account that grew from $10,000 carries exactly the same ruin risk at 20% position sizing as it would if you'd started with $15,000. The source of the capital is irrelevant to the mathematics of ruin.

2. Concentration Risk: The Position-Size Illusion

Traders who limit per-trade risk to 2% sometimes simultaneously hold 8-10 positions in correlated assets, creating a portfolio-level exposure that far exceeds their per-position risk budget. During correlated market stress events, these positions move together — producing real drawdowns of 15-20% from what appeared to be individual 2% risks.

3. Options Leverage Distortion

Options positions often represent far more than their dollar cost suggests. A $500 options position on 100 shares is economically equivalent to a $5,000 equity position. Traders who calculate position size based on premium paid rather than notional exposure systematically underestimate their actual risk and run ruin probabilities far higher than they realize.

Trade With Your Brain, Not Against It

Traderise includes built-in trading journals, risk controls, and psychology-aware features designed to help you make better decisions.

Try Traderise FreeA Practical Framework for Ruin-Proof Position Sizing

The 1-2% Rule Explained

The widely recommended rule — risk no more than 1-2% of total account per trade — is derived from ruin probability calculations. At 1% risk per trade with a 50% win rate and 1.5:1 R:R ratio, the probability of losing 50% of the account over 1,000 trades is approximately 0.003% — negligible for practical purposes. At 5% risk per trade, the same calculation produces an 11% ruin probability — mathematically significant over a trading career. Traderise's position calculator automatically translates your risk percentage into share quantities or contract sizes based on your current account value and defined stop level.

Tracking Your Personal Risk of Ruin

Use your actual performance statistics — not theoretical assumptions — to calculate your personal RoR regularly. If your win rate has been 48% over the last 100 trades with an average R:R of 1.3:1, your realistic edge is narrower than you might assume, and your position sizing should reflect that. Track these statistics in Traderise's analytics so you always have current, accurate inputs for your ruin probability calculations.

The Meta-Lesson: Longevity Is the Real Edge

The ultimate insight of risk of ruin mathematics is this: in trading, survival is strategy. The traders who achieve compounding growth over years are almost always those who prioritized surviving bad periods — not those who maximized returns during good ones. Every catastrophic blowup in retail trading history — and most professional ones — was preceded by position sizes that created unacceptably high ruin probabilities. The mathematics were always pointing to the outcome. The traders didn't look at the mathematics. Build your position sizing around ruin prevention first, return optimization second. The compounding of a modest, protected edge over years produces results that the big-bet, ruin-risk approach almost never does — because the big-bet approach rarely survives long enough to compound.

Make Mathematics Your Risk Manager

Traderise's position sizing tools, risk calculators, and hard exposure limits help you keep your Risk of Ruin at the manageable levels that allow long-term account growth.

Try Traderise Free